Sustainable Investing: Reimagining Products for Lasting Benefit

- Keywords:

- sustainable investing

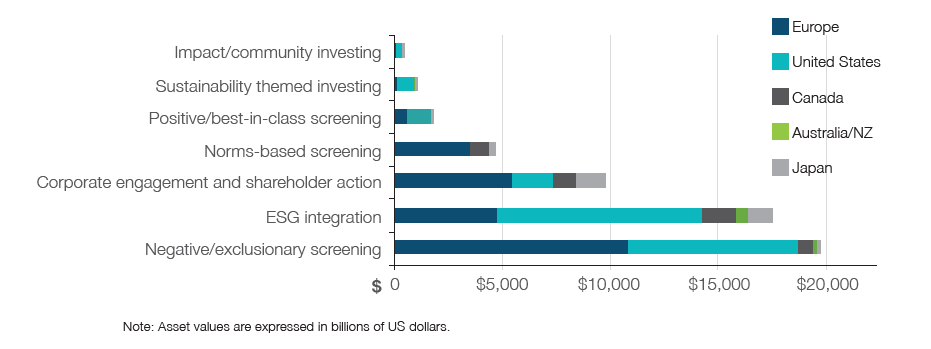

Every year, interest in sustainable investing continues to accelerate. Assets in sustainable investment-related products reached US$30.7 trillion at the start of 2018, up 34% from the beginning of 20161. Nearly 50% of assets in Europe while in Canada, Australia and New Zealand, more than half of all professionally managed assets were in at least one of the seven sustainable investing strategies. (Figure 1)

Of these seven strategies, impact investing has risen globally to US$500 billion2 today from $228 billion in 2018, with investors, entrepreneurs, corporations, foundations and nonprofits being the primary participants. More than half of these assets are managed by 800 asset managers who are seeking both financial returns and positive social impact.

The number of asset managers that have committed to socially responsible investing (SRI) and are incorporating environmental, social and governance (ESG) criteria is climbing too. In 2007, the United Nations Principles of Responsible Investing (PRI) was created, with BMO Global Asset Management being one of the 16 founding signatories. Now, more than 2300 managers, asset owners and service providers have signed on, while approximately 85% of the S&P 500 companies publish sustainability reports highlighting relevant ESG metrics that are utilized by the signatories.

“As it stands now, a diverse and robust suite of widely-accepted, liquid sustainable investing products do not exist today”

We also saw the introduction of novel investment products aligned with the U.N.’s 17 SDGs, including clean energy, women’s empowerment and a nonprofit ETF linked to the National Association for the Advancement of Colored People (NAACP). Anyone who has paid attention to this space won’t be surprised by the interest. With a growing focus on loss of biodiversity, building climate resilience, reducing food insecurity, and other global issues, people are becoming increasingly aware of how their actions – and the actions of the companies they invest in – impact the planet and its citizens. They want to see sustainable funds in their 401k plans, while more millennials and women, who are expected to hold more of the world’s wealth, are taking a greater interest in sustainable investing and increasingly looking for socially responsible products.

More products needed

It’s important to keep in mind that sustainable investing is one branch of sustainable finance and it’s not the only way that financial institutions can make a global impact. Ideally, corporations, asset managers, foundations, sovereign wealth funds and others should be adopting many facets of sustainable finance and aiming for a positive impact with every investment or financing. While sustainable investing is easier to understand than some other areas, it remains outside of the mainstream. Why? Because there aren’t enough and widely-accepted products on the market to drive demand and catalyse effective change. We are starting to talk about it, but we still have a long way to go.

In the U.S., the sustainable investment universe, which is comprised of open-end funds and exchange-traded portfolios, increased by 50% at the end of the 2018, with 351 funds holding a total of $160 Billion in assets3. While it’s good to see the numbers increasing, for sustainable investing to become mainstream, the breadth of products and the number of new fund launches must grow substantially.

Consider how assets are distributed among the seven sustainable investment strategies. About 65%, of global assets were in the negative or exclusionary screening strategy in 2018. While assets in the ESG integration strategy grew 69% year-over-year in 2018 to $17 trillion. (Figure 1)

Part of the reason why there are fewer investments in categories such as sustainability-themed or impact investing is that there aren’t enough products to satisfy the growing demand for sustainable investing. Sustainable investment products, including social bonds, green loans and ESG-themed mutual funds and ETFs are being developed, mostly, by re-purposing existing financial product structures that have existed in the industry for decades.

Figure 1: Sustainable investing assets by strategy 2018 (source GSIA)

Further, product developers often execute sustainable investing strategies by selecting a set of securities aimed towards positive impact, benefiting the environment and so on. Although corporations are an important force for effecting positive change, we cannot expect investments in these companies to be the sole source of positive impact on our planet since the class of the interconnected SDGs we are tackling to solve is highly complex.

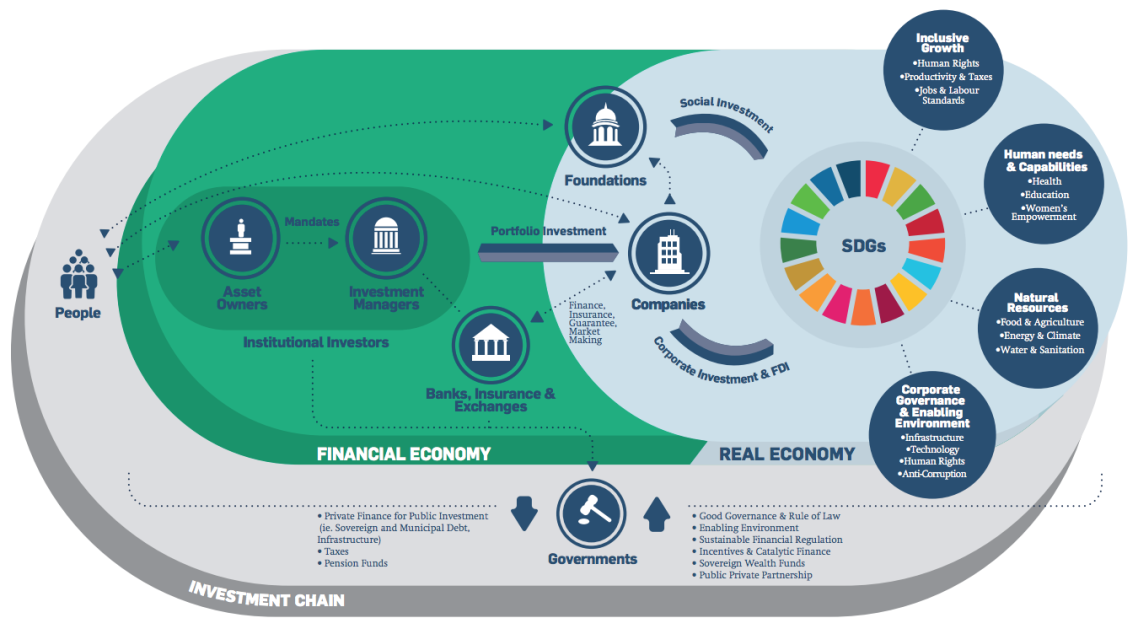

Creating broader investment opportunities needs to be a group effort where people are encouraged and rewarded to think outside of the box. Of course, building products that will yield financial return as well as a positive, measurable, social or environmental with a long-term benefit is no easy feat. As mentioned in Part One of the sustainable finance series, developing effective products requires systems thinking, which involves bringing different subject matter experts to the table, including scientists, policy-makers, economists and financial experts (Figure 2). You wouldn’t build a bridge with one skill set, so why would you build a complicated socially responsible investment product using a single expertise? Experts in poverty or climate change need to be developing new targeted products hand in hand with financial product developers in the future.

Unfortunately, developing and then adopting effective – and scalable – financial products can take decades. For instance, green bonds, which are underwritten to raise capital for projects that have an environmental impact, and now have more than US$600 billion issued worldwide, is a self-regulated industry. The lack of uniform standards, cohesive taxonomy and the laborintensive endeavors in setting up green bond programs are all deterrents to making this market grow at the pace needed for easy adoption by corporate issuers especially. Given the urgency around issues like climate change, social inequality and so on, we must work towards building and releasing SRI products into the market with pace.

Developing a more mature market

Leading institutions are implementing new ideas. In 2018, the Canadian Pension Plan Investment Board, which has $280 billion in AUM and was the world’s first pension fund to issue its own green bond, built a 20-member Power and Renewables Group that invests in early-stage projects, including in wind and solar, and invested more than $2.6 billion in its first year. In October 2018, Caisse de dépôt et placement du Québec partnered with Generation Investment Management, a sustainability-focused investment management firm, to invest $3 billion with 8 to 15 years duration in sustainable companies.

View larger image of graphic here

Figure 2: Eco-System for Financing SDGs (Source: UN Global Compact)

As well, more work is being done around the 17 SDGs. For instance, over the last four years funds focused on gender equality – both private and public investment vehicles – has jumped to over $5 billion4, from $100 million. As good as that may be, most of that money has gone into funds that support gender equality (SDG no. 5) in corporations, while products for other gender issues, such as eliminating violence, preventing early marriages or bringing access to financial inclusion to over a billion women, for institutional investors are lacking today in great numbers. Studies also show that at the current rate of change, the global gender gap will take 108 years to close.5 By accelerating the achievement of SDG no. 5, can we imagine a day where there would be large-scale tradeable liquid securities that address the gender gap and benefit women?

Despite the progress, for more products to take shape, whether it’s around gender equality or climate action and so on, market participants, including banks, need to increase adoption of the 17 SDGs by creating more innovative offerings for listed exchanges or by raising capital or financing companies. As it stands now, a diverse and robust suite of widely-accepted sustainable investing products designed for accomplishing the 17 SDGs or to serve those living in the Bottom of the Pyramid (BOP) – typically the poorest individuals – do not exist today.

Influences of the future

While it may take a while before a diverse set of experts are around the table and before targeted products are created and adopted in large numbers, there are signs that some asset managers are incorporating new methods of evaluation. For instance, some large asset managers are already analyzing climate data to understand how climate change will impact their investments and what risk adjustments are needed to its portfolios to be more climate-change ready.

Big data and machine learning will also push product development in the right direction. AI is proving to be a powerful tool for resource-intensive industries to monitor energy use, reduce waste or predict consumer demand and it will eventually lead to the development of new decarbonizing SRI products. There are asset managers emerging who have begun using machine learning to identify smart alpha and performance drivers for their ESG-integrated multi-asset funds, while TruValue Labs uses artificial intelligence (AI) to examine dynamic corporate data and uncover ESG behaviors, in real-time, that could have a material impact on a company’s value.

Over the next five years, the implementation of big data, machine learning and AI techniques will help bring sustainable investing more into the mainstream. These tools will help asset managers with risk mitigation, identify investable opportunities and allow them to distill ESG signals from noise. In addition, applying design thinking steps, from ideation to prototyping, will help financial firms build innovative and transformative investment products for SDGs and BOP.

Ultimately, people and SRI industry want to effect change by putting their wealth in products that matter to them. The sooner we can get together to think through these issues, leapfrog years of new product development, and come up with fresh investment options, the better chance we’ll have to grow impactful ESG assets and solve many of the world’s most pressing issues.

Click here to read the PDF.

Manju Seal is is Head of Sustainable Finance Advisory, BMO Capital Markets. She spearheads broader enterprise wide strategy and thought leadership around sustainable finance and investment considerations as well as ESG advisory within BMO Capital Markets. Manju leads efforts at BMO for sustainable/green bond underwriting, product development and financing activities while implementing client-focused strategies. She has over 20 years of diverse professional experience, including, investment banking, institutional asset management and nonprofit & board leadership.

1 GSIA 2 GIIN 3 Sustainable Funds U.S. Landscape Report 4 Sage & Veris reports 5 World Econ Forum

Read more

Manju Seal

Head of Sustainable Finance Advisory

Every year, interest in sustainable investing continues to accelerate. Assets in sustainable investment-related products reached US$30.7 trillion at the start of 2018, up 34% from the beginning of 20161. Nearly 50% of assets in Europe while in Canada, Australia and New Zealand, more than half of all professionally managed assets were in at least one of the seven sustainable investing strategies. (Figure 1)

Of these seven strategies, impact investing has risen globally to US$500 billion2 today from $228 billion in 2018, with investors, entrepreneurs, corporations, foundations and nonprofits being the primary participants. More than half of these assets are managed by 800 asset managers who are seeking both financial returns and positive social impact.

The number of asset managers that have committed to socially responsible investing (SRI) and are incorporating environmental, social and governance (ESG) criteria is climbing too. In 2007, the United Nations Principles of Responsible Investing (PRI) was created, with BMO Global Asset Management being one of the 16 founding signatories. Now, more than 2300 managers, asset owners and service providers have signed on, while approximately 85% of the S&P 500 companies publish sustainability reports highlighting relevant ESG metrics that are utilized by the signatories.

“As it stands now, a diverse and robust suite of widely-accepted, liquid sustainable investing products do not exist today”

We also saw the introduction of novel investment products aligned with the U.N.’s 17 SDGs, including clean energy, women’s empowerment and a nonprofit ETF linked to the National Association for the Advancement of Colored People (NAACP). Anyone who has paid attention to this space won’t be surprised by the interest. With a growing focus on loss of biodiversity, building climate resilience, reducing food insecurity, and other global issues, people are becoming increasingly aware of how their actions – and the actions of the companies they invest in – impact the planet and its citizens. They want to see sustainable funds in their 401k plans, while more millennials and women, who are expected to hold more of the world’s wealth, are taking a greater interest in sustainable investing and increasingly looking for socially responsible products.

More products needed

It’s important to keep in mind that sustainable investing is one branch of sustainable finance and it’s not the only way that financial institutions can make a global impact. Ideally, corporations, asset managers, foundations, sovereign wealth funds and others should be adopting many facets of sustainable finance and aiming for a positive impact with every investment or financing. While sustainable investing is easier to understand than some other areas, it remains outside of the mainstream. Why? Because there aren’t enough and widely-accepted products on the market to drive demand and catalyse effective change. We are starting to talk about it, but we still have a long way to go.

In the U.S., the sustainable investment universe, which is comprised of open-end funds and exchange-traded portfolios, increased by 50% at the end of the 2018, with 351 funds holding a total of $160 Billion in assets3. While it’s good to see the numbers increasing, for sustainable investing to become mainstream, the breadth of products and the number of new fund launches must grow substantially.

Consider how assets are distributed among the seven sustainable investment strategies. About 65%, of global assets were in the negative or exclusionary screening strategy in 2018. While assets in the ESG integration strategy grew 69% year-over-year in 2018 to $17 trillion. (Figure 1)

Part of the reason why there are fewer investments in categories such as sustainability-themed or impact investing is that there aren’t enough products to satisfy the growing demand for sustainable investing. Sustainable investment products, including social bonds, green loans and ESG-themed mutual funds and ETFs are being developed, mostly, by re-purposing existing financial product structures that have existed in the industry for decades.

Figure 1: Sustainable investing assets by strategy 2018 (source GSIA)

Further, product developers often execute sustainable investing strategies by selecting a set of securities aimed towards positive impact, benefiting the environment and so on. Although corporations are an important force for effecting positive change, we cannot expect investments in these companies to be the sole source of positive impact on our planet since the class of the interconnected SDGs we are tackling to solve is highly complex.

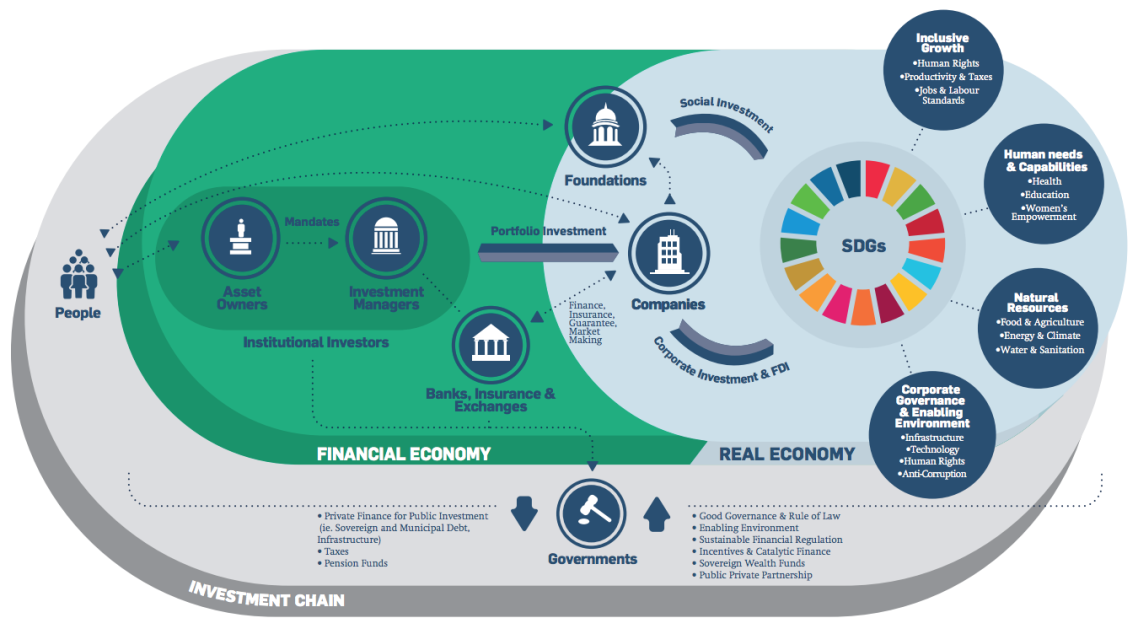

Creating broader investment opportunities needs to be a group effort where people are encouraged and rewarded to think outside of the box. Of course, building products that will yield financial return as well as a positive, measurable, social or environmental with a long-term benefit is no easy feat. As mentioned in Part One of the sustainable finance series, developing effective products requires systems thinking, which involves bringing different subject matter experts to the table, including scientists, policy-makers, economists and financial experts (Figure 2). You wouldn’t build a bridge with one skill set, so why would you build a complicated socially responsible investment product using a single expertise? Experts in poverty or climate change need to be developing new targeted products hand in hand with financial product developers in the future.

Unfortunately, developing and then adopting effective – and scalable – financial products can take decades. For instance, green bonds, which are underwritten to raise capital for projects that have an environmental impact, and now have more than US$600 billion issued worldwide, is a self-regulated industry. The lack of uniform standards, cohesive taxonomy and the laborintensive endeavors in setting up green bond programs are all deterrents to making this market grow at the pace needed for easy adoption by corporate issuers especially. Given the urgency around issues like climate change, social inequality and so on, we must work towards building and releasing SRI products into the market with pace.

Developing a more mature market

Leading institutions are implementing new ideas. In 2018, the Canadian Pension Plan Investment Board, which has $280 billion in AUM and was the world’s first pension fund to issue its own green bond, built a 20-member Power and Renewables Group that invests in early-stage projects, including in wind and solar, and invested more than $2.6 billion in its first year. In October 2018, Caisse de dépôt et placement du Québec partnered with Generation Investment Management, a sustainability-focused investment management firm, to invest $3 billion with 8 to 15 years duration in sustainable companies.

View larger image of graphic here

Figure 2: Eco-System for Financing SDGs (Source: UN Global Compact)

As well, more work is being done around the 17 SDGs. For instance, over the last four years funds focused on gender equality – both private and public investment vehicles – has jumped to over $5 billion4, from $100 million. As good as that may be, most of that money has gone into funds that support gender equality (SDG no. 5) in corporations, while products for other gender issues, such as eliminating violence, preventing early marriages or bringing access to financial inclusion to over a billion women, for institutional investors are lacking today in great numbers. Studies also show that at the current rate of change, the global gender gap will take 108 years to close.5 By accelerating the achievement of SDG no. 5, can we imagine a day where there would be large-scale tradeable liquid securities that address the gender gap and benefit women?

Despite the progress, for more products to take shape, whether it’s around gender equality or climate action and so on, market participants, including banks, need to increase adoption of the 17 SDGs by creating more innovative offerings for listed exchanges or by raising capital or financing companies. As it stands now, a diverse and robust suite of widely-accepted sustainable investing products designed for accomplishing the 17 SDGs or to serve those living in the Bottom of the Pyramid (BOP) – typically the poorest individuals – do not exist today.

Influences of the future

While it may take a while before a diverse set of experts are around the table and before targeted products are created and adopted in large numbers, there are signs that some asset managers are incorporating new methods of evaluation. For instance, some large asset managers are already analyzing climate data to understand how climate change will impact their investments and what risk adjustments are needed to its portfolios to be more climate-change ready.

Big data and machine learning will also push product development in the right direction. AI is proving to be a powerful tool for resource-intensive industries to monitor energy use, reduce waste or predict consumer demand and it will eventually lead to the development of new decarbonizing SRI products. There are asset managers emerging who have begun using machine learning to identify smart alpha and performance drivers for their ESG-integrated multi-asset funds, while TruValue Labs uses artificial intelligence (AI) to examine dynamic corporate data and uncover ESG behaviors, in real-time, that could have a material impact on a company’s value.

Over the next five years, the implementation of big data, machine learning and AI techniques will help bring sustainable investing more into the mainstream. These tools will help asset managers with risk mitigation, identify investable opportunities and allow them to distill ESG signals from noise. In addition, applying design thinking steps, from ideation to prototyping, will help financial firms build innovative and transformative investment products for SDGs and BOP.

Ultimately, people and SRI industry want to effect change by putting their wealth in products that matter to them. The sooner we can get together to think through these issues, leapfrog years of new product development, and come up with fresh investment options, the better chance we’ll have to grow impactful ESG assets and solve many of the world’s most pressing issues.

Click here to read the PDF.

Manju Seal is is Head of Sustainable Finance Advisory, BMO Capital Markets. She spearheads broader enterprise wide strategy and thought leadership around sustainable finance and investment considerations as well as ESG advisory within BMO Capital Markets. Manju leads efforts at BMO for sustainable/green bond underwriting, product development and financing activities while implementing client-focused strategies. She has over 20 years of diverse professional experience, including, investment banking, institutional asset management and nonprofit & board leadership.

1 GSIA 2 GIIN 3 Sustainable Funds U.S. Landscape Report 4 Sage & Veris reports 5 World Econ Forum

Tell us three simple things to

customize your experience

{kind=link}